Cheapest Book Multiple in 20 years, trading at 4.4x FCF

Net cash, asset backing and double‑digit shareholder yield

The Pitch

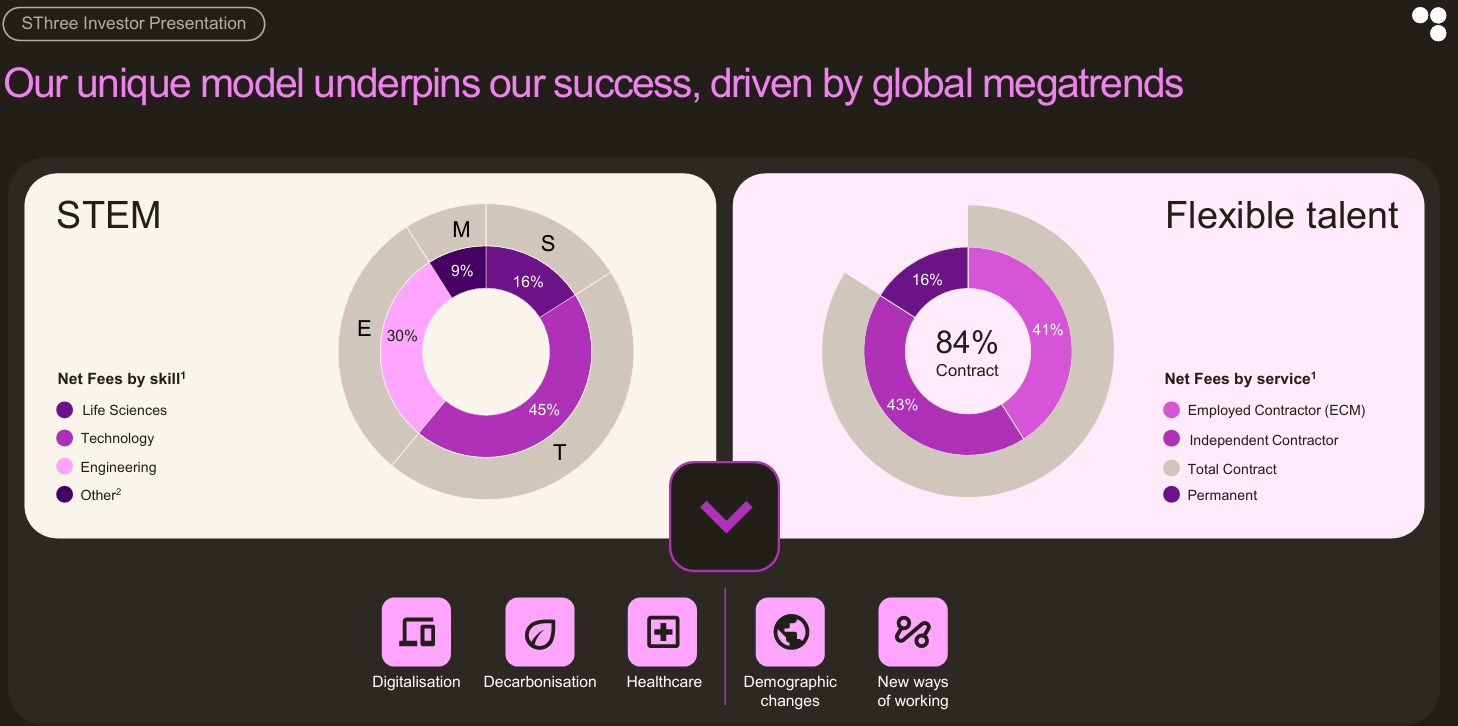

SThree is a global STEM recruitment and workforce-solutions business with a contractor dominant model, focused on engineers, technologists and life-sciences specialists. They are diversified in markets across Europe, USA and the Middle East & Asia.

It’s down 72% from all-time-highs, now valued like it is structurally impaired. I’d argue most of the damage looks cyclical: net fees have been hit by weak European hiring, while the contract book, pricing, and cash generation have held up better than the profit line suggests.

At a £207m market cap against £235m of net assets, and £51m of net cash, the shares trade below tangible book for a business that has remained free-cash-flow positive even in a downturn.

This works if Europe simply stops getting worse, management converts the completed technology programme into lower costs and better consultant productivity, and sizable capital returns continue while the market regains confidence in mid-cycle earnings power.

The Business & Situation

For readers who saw my recent piece on Kelly Services (which is pleasing to see up 25% in a month since), this will feel familiar: another cyclical recruiter, out of favour, trading below tangible book with a cleaner balance sheet than its share price implies. In SThree’s case, the asset backing, contract-heavy mix, insider buying and ongoing buybacks rhyme strongly with that earlier Kelly setup.

In simple terms, SThree helps companies hire hard-to-find STEM talent, especially contractors, and increasingly offers more complex workforce solutions where it handles compliance, payroll and delivery infrastructure as well as matching people to jobs. The contractor nuance is fairly important as it is more recurring and visible than permanent placements. Contract recruitment represents 83% of fees, with about five months of future fees sitting in the contractor order book (currently worth £152m)

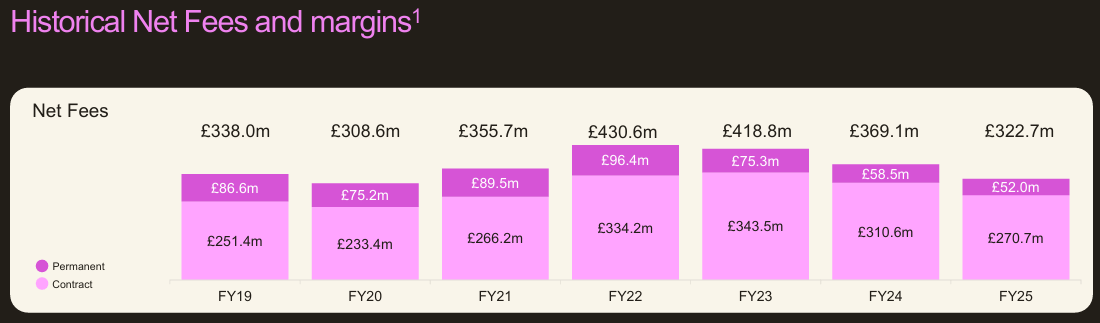

The stock is in the bargain bin because profits have collapsed, but the balance sheet is good. FY25 net fees fell 12% and operating profit fell 60% to £26.1m as weak hiring demand in Europe, especially Technology in Germany and the Netherlands, hit volumes while the company still carried a meaningful fixed cost base and higher IT costs after rolling out its Technology Improvement Programme (TIP).

The Asset Case

The asset case is the reason I am here, assessing downside first. Last reported figures give £235m of net assets, including £51m of net cash (latest RNS), £148m of net working capital, and only £16m of intangibles; that implies tangible net assets of roughly £219m.

P/TB = 0.95x

Here is a 20-year chart of market cap (blue) and tangible equity (purple), showing how drastic this current dislocation is.

The second chart shows the P/TB ratio - well below historic norms. For a deep-value investor, that means the market is offering a cash-backed operating business for less than the value of the tangible balance sheet, despite the company staying profitable and generating £47m of free cash flow in FY25 (4.4x P/FCF)

If we’re wrong on the cycle, investors still owns a business with real cash, receivables tied to ongoing contractor placements, and an undrawn £50m revolving credit facility. This is not a classic net-net, but it has some of the same appeal as a disliked cyclical trading near liquidation-style asset value, without balance-sheet stress.

Catalysts & Re-rating Path

The first catalyst is simple stabilisation. Q1 FY26 net fees were down 8% year on year, better than the prior run-rate, with the US and Japan growing, contract renewals resilient, and management reiterating full-year expectations. If that pattern persists, the market can start valuing SThree on trough-to-mid-cycle earnings rather than extrapolating a downturn indefinitely.

Second, their large IT Programme has moved from the spending phase to harvesting phase. Management says rollout finished on time and on budget across all 11 countries, with £6.5m of annualised cost efficiencies already delivered, and evidence of better consultant productivity, faster placement times, and stronger pipeline quality in markets where the system has bedded in.

Third, capital allocation: despite weak profits, the board maintained the dividend and launched another £20m buyback (on top of a previous £20m), which is exactly what an asset-backed company trading below tangible book should be doing if cash generation remains intact. That’s 20% of the float being bought back.

The dividend (8.5% yield) and the aggressive buybacks, results in a very high shareholder yield. Investors are getting both a cash coupon and material capital reduction.

Not a catalyst, but insider buying is also what I love to see. The CEO has bought ~£56k, the CFO with ~£35k, and a NED with £18k. Of course I’d prefer these were bigger, but still a positive sign and insiders still only buy for one reason…

Risks & What Could Go Wrong

The biggest risk is that this is not just cyclical. If European STEM hiring remains structurally weaker, or if clients increasingly internalise hiring and reduce reliance on recruiters, then “normal” margins may be permanently lower than history suggests.

The second risk is balance-sheet quality. A large part of tangible assets is working capital tied to receivables and contract assets, so a deeper downturn, client failures, or operational missteps in collections could erode book value.

The thesis breaks if SThree proves to be structurally, not cyclically, impaired, meaning net fees never recover much beyond today’s levels and margins fail to get back into at least low‑teens. It also breaks if working‑capital quality deteriorates (credit losses, bad debts, or persistent collection problems), turning today’s asset backing into a mirage rather than a genuine margin of safety.

Valuation & Expected Return

A sensible downside case is around stressed tangible book. If tangible equity of roughly £219m is haircut for troubled receivables and some operational drag, perhaps the business is worth around £170m-£180m, which suggests limited downside from the current market value.

A base case using a tangible book multiple feels a little off. It’s good for forming a view on the downside but as you can see from the second chart presented earlier, this company usually trades in a range well above here, between 2x-10x book. Sales or earnings might be cleaner to use.

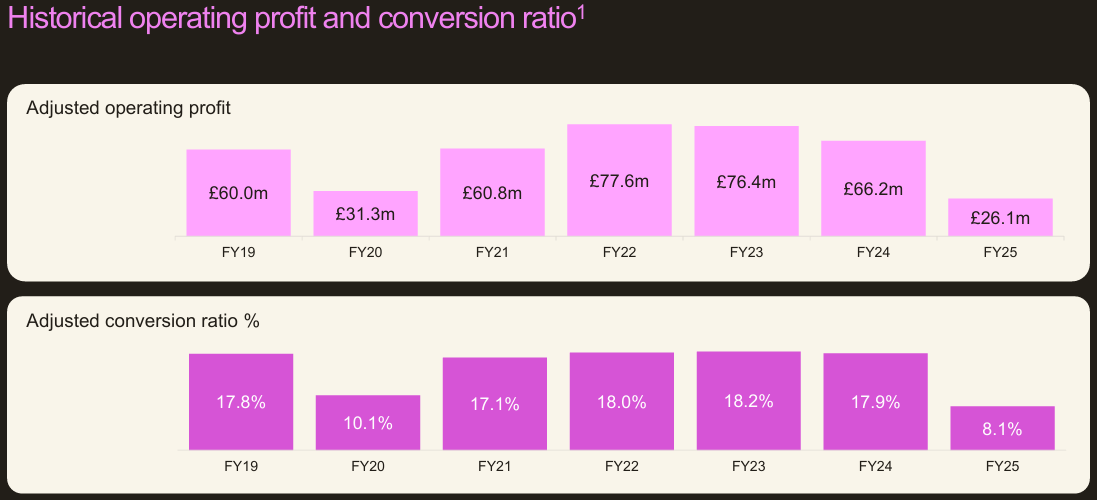

Over the last cycle SThree has typically earned operating margins in the high-teens, with FY19-FY24 operating‑profit conversion ratios between about 17% and 18% (excluding the 2020 pandemic dip) versus 8.1% in FY25. That tells you FY25 is a depressed point in the cycle, not anything like normal profitability.

A reasonable “mid‑cycle” net-fee level is somewhere between the 2019–2024 average and FY25: say £350m-£380m

Margin profiles:

Depressed: 10% (a step up from 8.1% now, but below history)

Mid: 13-14% (still below the 17-18% seen in the last upcycle)

Optimistic: 15-16%

On an assumed £360m of net fees at a 13% margin, operating profit is ~£47m, with post costs and tax profits coming around £34m. At a fairly conservative 10x multiple, a market cap of £340m. An upside of 65%.

With a more optimistic outlook: SThree earned £66.2m of operating profit in FY24 and over £76m in FY22–FY23, while management now argues that TIP should support sustainably higher margins over time. Even a partial recovery toward mid-cycle earnings, say around £60m operating profit and therefore ~£43m net income should justify a materially higher multiple. At 14x, you’d come in around £600m; a near treble upside from today’s £207m.

A treble sounds alarming, but feels plausible if Europe stabilises, the US keeps growing, and TIP benefits turn visible. It’s also worth noting the market cap was £810m in 2021. There’s attractive upside with an asset-backed floor.

CEO snippets from the recent earnings calls seem promising too: “We are witnessing ongoing stabilisation… with sustained momentum in both the U.S.A. and Japan… This improvement… underscores a marked increase in productivity and enhanced operational efficiency” and “While it’s too early to call a broad‑based sustained recovery, we remain cautiously optimistic…”

Conclusion

SThree is a cyclical recruiter with ugly recent numbers. However, it wouldn’t be on my screen if it wasn’t and that is exactly why it sits in the kind of territory deep-value investors should care about: now below tangible book for the first time in 20 years, net cash backed, still FCF generative, buying back stock, insider buying and one turn in the cycle away from looking much less broken.

I think this has good upside with limited downside, given tangible asset backing and cash.

Disclaimer:

These write-ups aren’t month-long research reports and could omit material information, so I always welcome feedback. As always, please do your own research.

The companies discussed often involve complexity or risk, and outcomes can vary widely. Investing in small/micro-cap stocks carries a high risk of capital loss.

The author may hold a long position at the time of writing. The author may buy or sell shares in this company at any time without further notice. This post is for informational and educational purposes only and does not constitute financial advice.

Great piece, and as a value investor, focusing in on what I often look for. A company so depressed valuation wise, that even if maintains it's reduced/distressed 'state' will deliver value/dividend income over the mid to medium term that will exceed the mkt cap/SP purchase price. Thanks for taking the time to write this.

nice, what about ai disruption/productivity risk?