Boring Infrastructure; Exciting Capital Returns

A 100% total-return machine, with an activist nudge.

The Pitch

Sekisui Jushi (4212) is a dull road‑safety and infrastructure supplier sitting on a fortress balance sheet that earns reasonable growing returns, yet trades below its tangible assets. With activist NAVF also pressing for continued shareholder friendly capital allocation and cross‑shareholding unwinds, investors are paid in buybacks and dividends while they wait for the gap to close.

Market cap 64.5bn

Tangible equity 82bn

The Business and Situation

Sekisui Jushi builds the physical plumbing of modern roads, towns and logistics. It makes soundproof walls for highways/railways, lane dividers, guardrails, protective fences etc, amongst a bunch of other things like artificial turf for sports fields, and privacy fences/walls for homes and factories. There’s other areas too like plastic strapping, packaging machinery, agricultural materials and wildlife‑damage prevention products. So many things that would bore you if I list them all!

It’s a dull Japanese industrial.

The customers are institutional and commercial: national and local governments, highway and rail operators, construction firms, logistics, agricultural operators etc. They’re essentially a fixtures and safety hardware provider, with decades‑long relationships and a diverse base.

The Fundamentals

Firstly, there’s nothing particularly novel about a Japanese industrial trading below book value, however this one spiked my interest given the business seems to have turned a corner, both in terms of operational performance (after some mildly troubled M&A) and a very clear commitment to shareholder returns they are executing on.

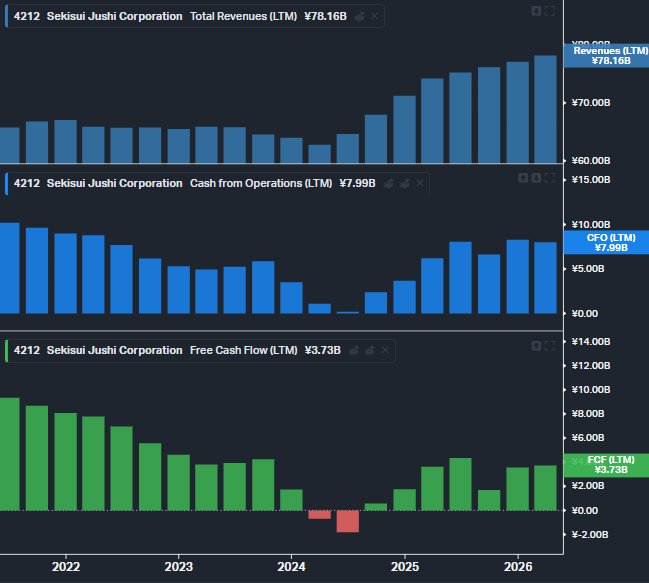

Here is a snapshot below of the last 5 years. Sekisui has grown revenue from about 65bn to 78.1bn, as of results released this month. Acquisitions have helped drive this.

Profits have been volatile, as raw‑material, transport/energy costs spiked and management leaned into M&A and growth investments/Capex. There’s been plenty of near term margin disruption and transitional headwinds, especially through an accounting lens.

That should now be in the rear-view mirror. 2026 results, which have just come out, show a strong rebound and stabilisation, with growth now back on the agenda. Op profit came in 13% stronger, net income 12% stronger, and margins ticking up.

Operating cash flow is very solid and has increased from 6.2bn to roughly 8bn (about +29%), driven by price revisions, cost‑cutting and higher EBITDA from both existing operations and the recent acquisitions. Free cash flow before financing has moved from 2.8bn to 3.8b – a robust increase of around 35% year on year.

FY27 guidance: revenue 84bn (up 7.5%), operating profit 6.3bn (up 11%), net profit 4.4bn (up 11%). i.e. a third consecutive year of record revenue and further profit growth. Things are now going in the right direction.

Napkin maths = 6 x EV/EBITDA (EV 59b to 9.7b EBITDA). So a cheap multiple, with teen growth in profits for the foreseeable future. It also trades near decade lows from a P/S perspective as shown below (often a cleaner valuation measure to look through messy accounting).

Not bad so far, but probably not enough to make you lean forward.

The cash flows show this is a robust business, but the balance sheet and intended plans for it is what turns this from “reasonably cheap industrial” to something more attractive.

Equity stands ~101bn, tangible ~82bn, with of most interest:

23bn of long‑term deposits

17.3bn of investment securities (cross-holdings)

18.3bn of cash

22.5bn PPE

Total liabilities of 41.5bn, of which short‑term borrowings have recently dropped from 12.3bn to 5.9bn. They have issued 4.7bn of bonds and increased long‑term borrowings. That gives them ample ammunition to hit the buyback and cross‑shareholding‑reduction goals without stressing the operating business (which I will come onto shortly)

So relative to today’s market cap of 64bn, it’s priced around 0.77x TBV.

Cheap on earnings, cheap on assets.

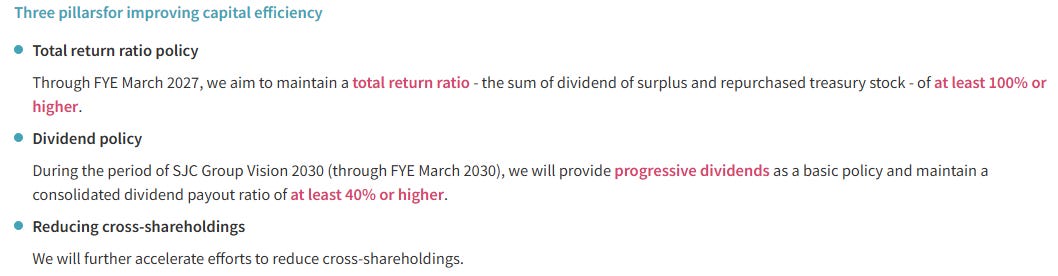

Moving on. The key bit that matters for this pitch: management is decisively shareholder‑friendly and is executing. Three explicit pillars in particular:

To break this down:

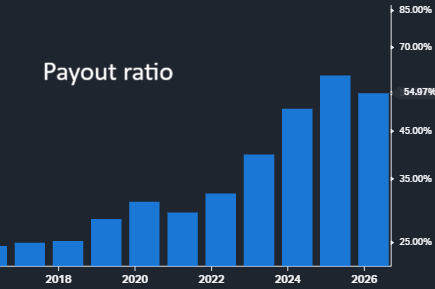

Dividends - The company has increased its dividend consecutively (up 14% this year) and now pays out more than half of earnings.

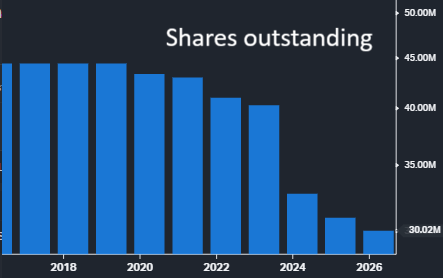

Buybacks - Repurchased 16.7bn in 2024, 4.2bn worth of shares in 2025, another 2bn worth in 2026 to date and 2.7bn further planned.

Cross-holdings - Management has committed to “further accelerate efforts to reduce cross‑shareholdings” - with a commitment to reduce by 30%; approx 5.2bn (based on 17.3bn holdings). This monetisation could be a huge windfall.

This is starting to look like a controlled self‑liquidation of non‑core financial assets over several years, overseen by activists rather than just a passive industrial.

On the recent earnings call, they explicitly state they can both fund growth and materially increase payouts without weakening the balance sheet.

On that activist point:

NAVF’s presence is an important kicker in this story, to keep the pressure on management to continue executing. It has built a meaningful stake since 2024, having publicly identified it as a classic engagement target: a solid, cash‑generative infrastructure business weighed down by cross‑shareholdings, surplus financial assets and a clumsy acquisition. In my view, NAVF are a serious outfit, as evidenced by their 24% CAGR performance since inception.

This new trajectory, from lazy balance sheet to activist‑nudged capital‑return vehicle, is exactly what makes this a live situation rather than just another cheap Japanese small cap.

What is the market missing?

The market sees a low ROE, small Japanese industrial with messy acquisition accounting and a troubled few years. It assumes it is just another capital‑inefficient conglomerate. ROE is only about 4%, weighed down by deals and a cocktail of transitional adjustments (it used to be nearer 8%). On lookback headline numbers at first glance, there is little to excite investors.

(FWIW, the 10-year CAGR including dividends is about 9%, so I wouldn’t harshly label it a melting value trap either)

What is under‑appreciated is that this “inefficiency” is precisely the ingredient that activists like NAVF are targeting; and we are seeing progress. Current profitability understates the underlying earning power once transitional headwinds pass. We are now seeing this in the 2026 and 2027 numbers, with double-digit growth in the guidance.

Sekisui is now doing all the things activists lobby for: committing to sell down cross‑shareholdings, shifting from hoarding to returning capital, and explicitly managing with an eye on cost of capital and share price.

What is my margin of safety?

The margin of safety comes from a combination of tangible assets and an emerging capital‑return machine. Investors are buying a debt‑light, cash‑rich industrial with stable public‑sector and commercial end‑markets.

On top of asset backing, shareholders are being paid out aggressively while they wait. A 100%+ total return ratio means that, absent a collapse in earnings, most of today’s earnings should come back via dividends and buybacks. For a deep value investor, that combination of tangible assets, conservative financing, and a clear capital return policy offers a wide buffer against permanent capital loss.

What gets the gap to close?

I am repeating the above, but to be succinct and clear:

Continued execution of the buyback and dividend policy

Visible reduction of cross‑shareholdings and long‑term investments

Modest improvements in ROE and margins (price increases, cost reductions, and acquisition integrations/synergies)

Pressure and public commentary from activist NAVF

What could go wrong?

This could still be a value trap. Management might talk a good game on capital efficiency yet stop short of truly slimming the balance sheet, leaving ROE stuck in the mid‑single digits and the stock perpetually cheap.

The activism angle is helpful but not decisive: NAVF is influential, not a silver-bullet.

Operationally, the risk is that acquisitions and growth projects consume more capital than they return - with planned synergies not as beneficial as hoped.

Sekisui Jushi will never be the sexiest name in a portfolio, but that is precisely the appeal. You have a niche but critical industrial, wrapped in a fortress balance sheet; run by a team that understands capital and shareholder returns.

Investors today can buy tangible assets at a discount, collect a rising stream of cash returns and wait for a more rational capital structure to be recognised. For a deep value investor willing to be patient, that is a perfectly acceptable way to compound.

Disclaimer:

I review lots of companies and write up a small bunch that I find interesting. These write-ups aren’t month-long research reports and could omit material information, so I always welcome feedback.

The companies discussed often involve complexity or risk, and outcomes can vary widely. This is what puts most investors off and is why they work collectively over the long term. I do not encourage extreme stock concentration.

Nothing here is investment advice or a recommendation. As always, please do your own research.

Those sure are some "Jushi" dividends 😂 👌

Thanks for this. I am a tourist, so just invest in NAVF, as they know more than me, but good to drill deeper into their portfolio.