A profitable net-net with a cash war chest

Priced for Liquidation, Positioned for Recovery

The Pitch

Nexteq is a specialist B2B technology outsourcer. It supplies the computing hardware and display systems that sit inside slot machines and industrial equipment such as broadcast panels and medical devices. The market is treating what may be hopefully be a temporary, exogenous earnings trough as permanent franchise damage.

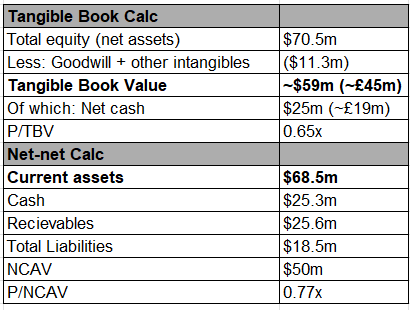

Now at ~55p, the stock trades at roughly 0.65x tangible book and as a classic net-net with a 0.77x NCAV ratio. There’s net cash of ~£19m representing two-thirds the entire market cap (£29.3m)

You’re acquiring the whole operating franchise for somewhere in the region of £10-11m implied enterprise value.

For the thesis to work, the gaming volumes need to partially normalise as tariff uncertainty fades and memory costs ease, and at least one of several nascent revenue streams needs to begin generating meaningful revenue.

None requires a return to peak, just a return to functional normality.

The Business & Situation

Nexteq runs two brands.

Quixant makes the computers inside casino slot machines. The largest gaming manufacturers build their own computers in-house, but when a mid-tier gaming manufacturer builds a new slot machine cabinet, there’s a reasonable chance it runs on a Quixant PC. Game developers design the games and Quixant handles the regulated, supply-chain-intensive hardware stack underneath. This is genuine outsourcing with 20 years of gaming compliance certifications, deep engineering relationships, and serious switching costs. Quixant is 67% of group revenue.

Densitron, which as a brand is over 50 years old, makes the display screens and control surfaces used by organisations like the BBC, CNN, medical device manufacturers, and industrial equipment makers. It has been pivoting from selling plain screens to selling complete integrated systems: computer + display + housing + software. A meaningfully more valuable and margin-accretive proposition. Densitron delivered a record-high gross margin of 38%+ in FY2025.

Why is it cheap?

I am often cautious to fit narratives to stock charts, but there’s been a number of things over the last few years that I’ve uncovered. A timeline works best:

2013-2018 - The glory days, Nexteq was a genuine AIM-market growth darling. It was doing something novel, convincing gaming manufacturers to outsource their computing rather than build it in-house and winning customer after customer.

2019 - This was the first crack and the cause is important: customer concentration risk crystallised for the first time. A small number of very large gaming manufacturers drove the majority of Quixant’s revenue, and when one or two of them had a poor year it hit Quixant disproportionately hard.

2020 - Casino floors globally shut down overnight. Gaming manufacturers stopped ordering. Revenues collapsed. Fairly self-explanatory. After the COVID damage, the business and stock saw a reasonable recovery, late 2020 through to 2023.

2023-2025 - Three years of pain:

Destocking - Gaming manufacturers over-ordered computers during the supply-chain chaos of 2021–22, then spent the next 18 months working through the excess rather than placing new orders.

Leadership exodus - In 2024, the founding CEO, CFO, and Chair all departed within a short window, the kind of concentrated senior exit that causes investors to head for the door. The incoming team inherited a destocking hangover and had to rebuild the management structure from scratch.

Everi - Nexteq’s largest gaming customer was acquired by private equity firm Apollo (who also bought IGT), which then rationalised its product range far more aggressively than anyone expected, hitting Nexteq very hard. Since then the business has replaced most of this lost work through new wins (e.g. Arrow International), but the uncertainty triggered back-to-back profit warnings.

From my understanding, each layer of bad news arrived when the market was already fragile on the stock. Then more recently, there’s been a memory shortage issue too. AI data centre buildout has hoovered up memory supply, which Quixant’s gaming PCs run on. Costs have inflated sharply.

There’s also been US tariff uncertainty. Whilst their own products are tariff-free, management state that tariffs have impacted the run rates of clients in the Gaming industry. Gaming cabinet components attract tariffs, suppressing operators’ confidence and order books.

As a result of these more recent issues, the recent management update warned FY2026 revenue will land ~15% below prior consensus ($85m to $73m). The stock fell further.

So, a rough few years. The market is now pricing the business as if it will never recover. But as a net-net stock, I am highly interested - particularly as there’s a reasonable set of opportunities for Nexteq ahead.

The Asset Case

Nexteq trades in the UK, but reports in USD.

At ~£29.3m market cap, NXQ trades at approximately 0.65x TBV. Strip out the cash and the market values the entire operating business: brands, customer relationships, patents, supply chain infrastructure, and ~£27m of real operating assets at roughly £10m.

Even applying a punishing 20% haircut to inventory and receivables for obsolescence and collection risk, adjusted TBV still comes out at ~£38-40m, comfortably above the current market price.

The business has generated net income and FCF for many years, suffering no years of losses, despite all that has gone on. It’s continued to raise dividends, and repurchased shares throughout. This is not a deteriorating asset base.

Catalysts & Re-rating Path

Net-nets are so cheap they often just find a way to make you money without a known catalyst upfront being required.

That being said, my analysis shows quite a few potential catalysts, which I’ve ranked in terms of their impact on a re-rating; prioritising immediate earnings recovery and tangible per-share value creation:

1. Memory costs normalise - For a depressed net-net, the fastest way to force a re-rating is a sudden normalisation of earnings. Nexteq has a largely fixed operating cost base, meaning that bridging the gap from a 32.8% gross margin back to the targeted 35-38% will drop a lot straight to the bottom line. This catalyst requires zero new customer wins, just pure operating leverage and the most mathematically certain driver of near-term EPS recovery.

2. IGT Opportunity - While the market has heavily penalised Nexteq for the abrupt volume decline following Apollo’s acquisition of Everi, this disruption has created a structural entry point into IGT. The merger combined Everi with IGT, a “Tier 1” giant that has historically kept its hardware manufacturing in-house. The silver-lining from it is the foot-in-the-door it’s given Nexteq. They’ve leveraged the merger to secure new, incremental business directly with IGT in Spain and Brazil. Winning broader IGT volume would not only replace that lost revenue but structurally upgrade Nexteq’s customer base into “Tier 1” territory.

3. Capital returns - When a stock trades at 0.65x tangible book value, aggressive share buybacks are heavily accretive. Combined with a 7% div yield, this capital allocation mathematically forces value upward while providing a tangible floor.

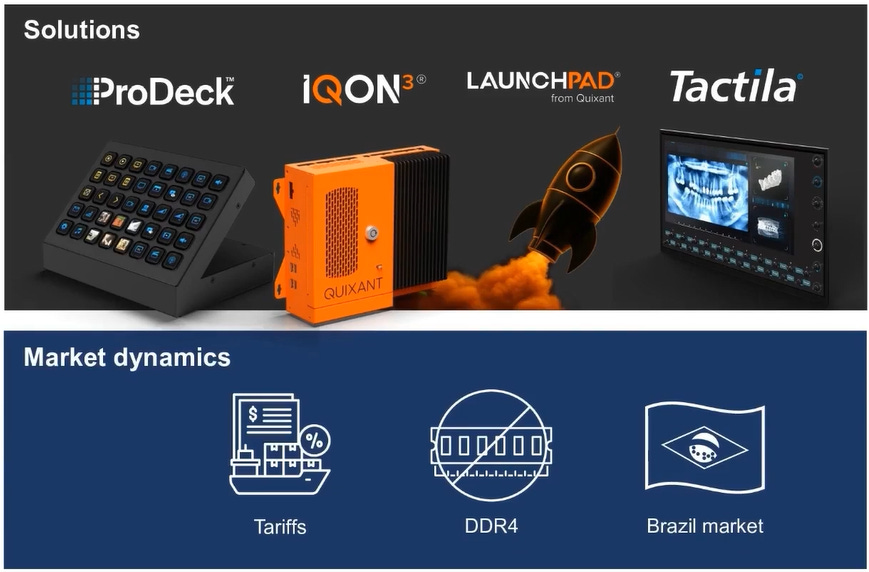

4. Product sales ramp up - Launchpad (new 2026 gaming platform) and Tactila (new broadcast solution) represent the transition from lower-margin hardware to sticky, high-margin software and integrated systems. A few early wins so far have validated this transition. Even modest traction here is a material re-rating story for a business priced for no growth.

5. Tier 3 Market Expansion - The Tier 3 market refers to the distributed route and amusement sector, comprising roughly 500,000 gaming cabinets outside of casinos in venues like bars and stores. Expanding the TAM by so much is attractive, but the impact is somewhat delayed/unknown. With purpose-built hardware for this market launching in late 2026, this is a 2027/2028 story but with large potential.

6. Brazil volumes emerge - Nexteq has started making traction in Brazil, an entirely new and incremental revenue stream with revenues expected in FY2026, and a market the company’s own CEO has flagged as a significant growth opportunity in 2027 and beyond. This is an exciting narrative and offers upside optionality. Perhaps viewed as a “call option” rather than a core thesis pillar today.

Risks & What Could Go Wrong

The Everi customer/volume loss situation was painful but recoverable. The question is whether something similar happens again. Nexteq’s model also relies on mid-tier gaming manufacturers choosing to outsource rather than build in-house.

Memory shortage runs longer than expected. If AI infrastructure buildout consumes memory supply for three or four years rather than one or two, the path to normalised margins extends.

M&A misallocation. With £19m of cash, a poorly-executed acquisition is the fastest way to destroy the balance sheet floor underpinning this investment. Management has commented they are actively looking.

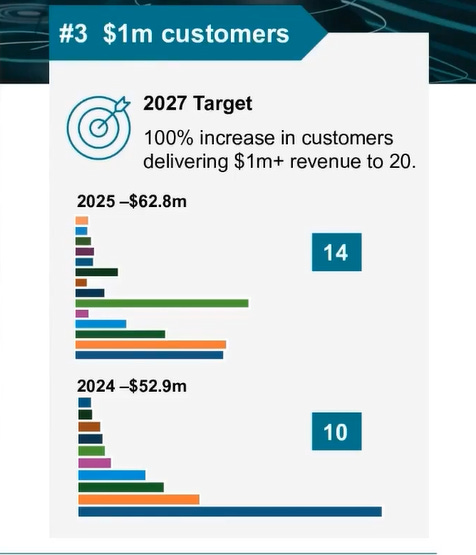

Thesis breaker: If any single large relationship deteriorates sharply, or if a key customer elects to bring computing in-house, the revenue base resets materially lower again. Will need to watch the customer diversification metrics (number of £1m+ customers as show below). You can see the Everi impact (dark blue line). Secondly, if net cash falls below ~£12m without a credible earnings recovery trajectory in sight, the balance of probabilities / margin of safety shifts materially.

Valuation & Expected Return

Probably best to look at this from several angles (sales, earnings and book) given the historically wide P/TB range.

Today the market cap is £29.3m at 0.65x P/TB and 0.4x P/S. If we take unheroic averages from the last few years:

Book: around 0.9x TBV or NCAV value = £38-40m. A ~40% upside

Sales: around 0.9x, on a recovery to a 2027 revenue of £70. A ~ 110% upside

Earnings: around 12x on a normalised net income of £5m. A ~100% upside

Given this is a net-net, the downside here is primarily time, not permanent capital loss (in my opinion), given the cash cushion. I’m not saying it can’t get cheaper, but on paper the downside looks limited from here.

I don’t want to get too cute or precise as there’s a lot of variables here. I think it’s really cheap and I think it’s worth approximately double on a base case, with downside buffered by assets that comfortably exceed today’s market cap.

Nexteq had a peak market cap of over £300m pre-pandemic (today it’s £29.3m). I’m not arguing this is a potential ten-bagger, but you can see the potential if demand and profits “normalise” / return.

This one probably requires patience and the stomach for near-term earnings disappointment. But the franchise is intact (it’s never made a loss), insider alignment is genuine (38% insider ownership), and numerous new revenue streams are promising.

When something is this cheap, it has a habit of finding a way.

Disclaimer:

These write-ups aren’t month-long research reports and could omit material information, so I always welcome feedback. As always, please do your own research.

The companies discussed often involve complexity or risk, and outcomes can vary widely. Investing in small/micro-cap stocks carries a high risk of capital loss.

The author may hold a long position at the time of writing. The author may buy or sell shares in this company at any time without further notice. This post is for informational and educational purposes only and does not constitute financial advice.